Life insurance quotes are based on one’s age (usually nearest), gender, and smoking status. Personal and family health history also determines whether a policy will be issued at standard rates, a higher cost or even a decline. There are other factors that may impact eligibility such as one’s driving record (speeding tickets, suspended licence), past drug usage, criminal record, bankruptcy and engaging in hazardous sports. Regardless of your personal situation, by honestly answering the questions, we will be able to find the best options for you.

If you pass away, how will your family continue to pay the rent or mortgage? Would your family be able to replace your income to maintain their lifestyle? How would you feel, knowing that your funeral expenses are not going to cause a financial burden for others?

Would you like to use life insurance to donate to a charity? Did you know that life insurance can also be another asset for you? Life insurance can accumulate cash value (tax deferred). Do you have a mortgage or a loan and the creditor requires insurance in case you pass away? Did you know that you can use an individually owned policy to meet this requirement and the cost and benefits to you are far greater than that offered by the financial institution?

The beneficiaries receive the life insurance proceeds as tax free dollars. How long would it take you to save $25,000, $50,000 or $100,000? Whatever your number is, you will be surprised to see the cost for life insurance is affordable. By using life insurance effectively, you can change the financial prospects for your children or grandchildren. You do not have to be rich to leave a legacy.

Guaranteed Issue Life Insurance

Have you been declined for life insurance? Have you been recently diagnosed with cancer, experienced a heart attack, stroke or other illness? There are zero medical questions and no medical tests.

Usually in the first two years, if death occurs (other than by accidental means) the premiums paid will be received by the beneficiary. Some insurance companies will also pay an interest amount as well. After two years, the full coverage will be paid whether death is by accidental means or not. These policies are usually issued instantly and coverage begins as soon as the initial premium is paid.

Coverage is for life and premiums remain the same for life (usually age one hundred). Available options provide cash value or the ability to stop paying and maintain a reduced paid up amount of insurance. Coverage amounts vary from $5,000 to $100,000.

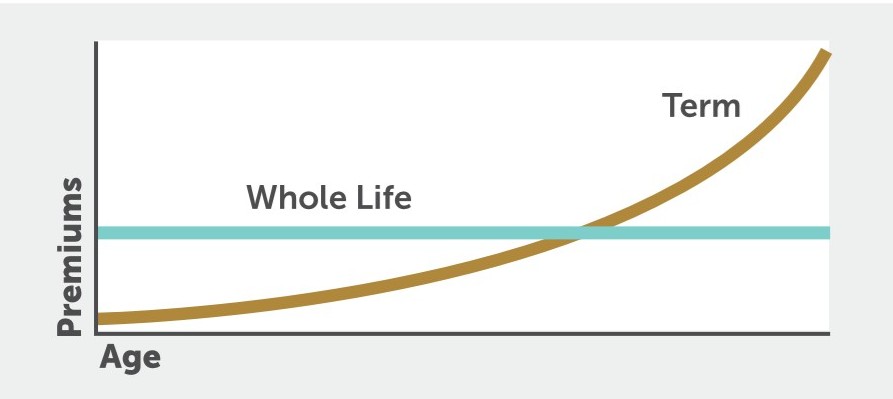

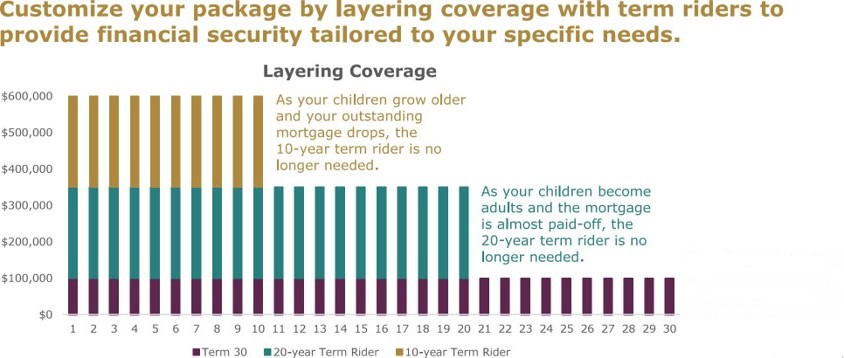

Renewable and Convertible Term Insurance

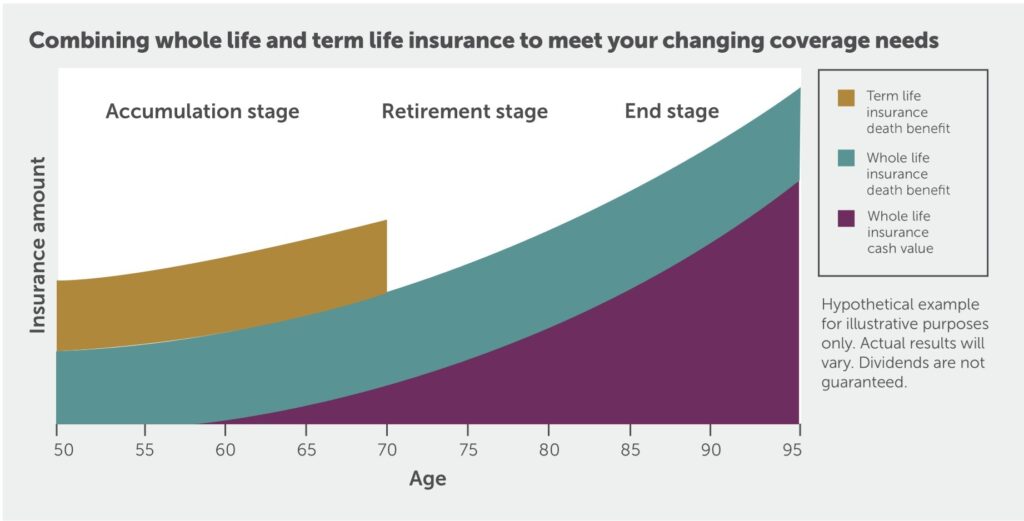

Coverage is like car insurance; it only pays if there is a claim. There are no savings or cash associated with these policies. Various lengths of terms are available, for example, 10, 20 or 30 years. The length of the term determines how long the premium will remain the same. The policy will automatically renew at a significantly higher rate or you can choose to decrease coverage or cancel it.

Your health situation could drastically change by the end of your term and you may not be eligible for a new policy. The conversion option is priceless in this scenario. You can choose to switch to a permanent product that the insurer offers with coverage up to the amount you are covered for. There are no required medical tests, or questions.

To help you understand how valuable such coverage is, imagine if you were to apply to rent a property from the builder. After answering all the questions and providing necessary information, your lease is approved for twenty years. In addition, the builder includes in your agreement that at any point you can choose to purchase the property based on the market value at that time, without having to qualify for the mortgage.

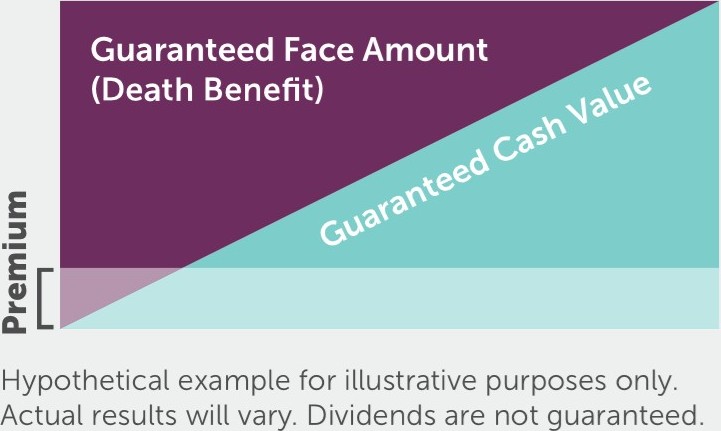

Whole LIfe

Coverage is permanent (for life, usually to age 100) and the premium remains the same. Options for limited payments are available. For example, a 20 Pay policy would require payments for 20 years but coverage would continue for life.

Non-Participating Whole Life Insurance

Contractually provides a guaranteed cash surrender value. The longer the policy is in force the greater the value. If circumstances no longer require you to keep this policy, you can surrender it and take the cash. The cash value can also be borrowed; you do not have to qualify to access these funds like when applying for a loan at the bank. Depending on the amount of the cash value, you can choose when and if you would like to make payments toward the loan.

Some policies contractually allow you to stop making premium payments with a reduced coverage amount.

Participating Whole Life Insurance

Same features as the non-participating plan with the inclusion of dividend options.

Many of these policies have limited pay options like 10, 15 or 20 Pay (Pay premiums for that period then payments stop but coverage continues for life). Some are designed to grow the cash value at higher amounts in the early policy years.

Here are some of the available dividend options offered:

Cash Payment: Dividends are paid directly to you and may add to your taxable income.

Premium Reduction: Use your dividends to cover your premiums. If your dividends are greater than the premiums due, they remain on deposit and may earn interest.

Dividends on Deposit: Dividends stay on deposit and can potentiality earn interest. They can be withdrawn at any time, subject to taxation.

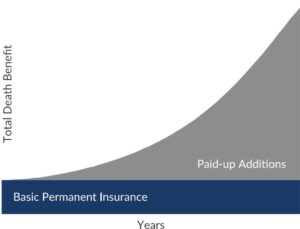

Enhanced Dividend Option: Your policy begins with a combination of basic permanent coverage, which is what your premium payments purchase, and yearly renewable one-year term insurance coverage (Enhancement, which is what dividend payments purchase). Dividend payments are used first to pay for the one-year term insurance with any excess used to purchase participating paid-up additional insurance. Any new paid-up additional insurance automatically replaces part of the one-year term insurance. Once all the original one-year term insurance has been replaced with paid-up additional insurance, the dividend conversion point is reached. At this point, any future dividend payments are used to purchase paid-up additional insurance, which increase the amount of the death benefit.

If the enhanced dividend option is selected, a policy with a lifetime guarantee is recommended.

Paid-Up Additions: This option uses dividend payments to purchase participating paid-up additional insurance. Paid-up additional insurance is added to the basic policy to create another “layer” of permanent participating whole life insurance, which is also eligible to participate in the earnings of the participating account through dividend payments. Dividend payments on paid-up additional insurance, combined with dividend payments on your basic permanent coverage, can result in increases in both the death benefit and cash value over the life of your policy. The cash value of paid-up additional insurance grows on a tax-advantaged basis.

Universal Life Insurance

This policy contains an insurance component and a savings component. There is a wide selection of segregated funds to choose from, as well as guaranteed interest options, to meet different investor profiles. The investment portion grows tax deferred until withdrawn. At time of claim, both the insurance amount and total value of the investment portion, are paid out to the beneficiaries tax free.